Retirement (as well as education and the job market) is one of our greatest future-unknowns.

We know it will happen… but we are finding it harder to understand and predict what it might look like. This doesn’t mean we should abandon planning for it. If anything, it simply means that we need to change the way we start to talk about, engage with and plan for retirement.

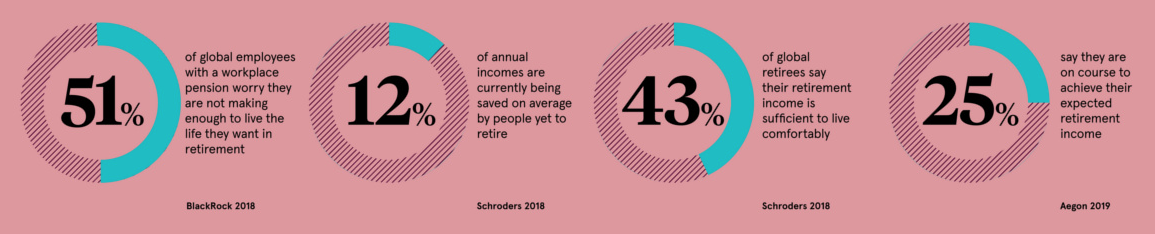

According to a global survey done by BlackRock, about 51% of the world’s working population, worry that their workplace pension will not cover the retirement life they want. This is why most people have a dim view of retirement. But this view is mostly framed by the conversation that retirement is meant to be a welcome reward following a successful working career. In other words, we work for about 45 years, and then we take a 20 year paid vacation….

The biggest problem with this picture is that very few people are able to save for that full 45 year period, and even fewer manage to avoid having to draw on these savings for unforeseen expenses ahead of their retirement.

That’s why we have a rap about the gap that’s not very helpful.

If we are to change this conversation and try to gain a more helpful understanding of retirement, we need to find out how to ask better questions.

How are you shaping your expectations for retirement?

A Schroders 2018 survey, showed that people usually receive less than what they expected their retirement income to be. It is important to know how much you will receive as this needs to align with your planning and your expectations. Whilst retirement is not only about how much you will earn, it’s important to know what you will have to work with.

If you would like to have the opportunity to study further, open a new business, pursue new hobbies, travel or live abroad, planning for a renewable income as well as new income sources is important.

The same Schroders survey also found that 43% of global retirees, who said their income was less than expected, still felt like their retirement income was sufficient to live off comfortably.

Some people continue working into their retirement years; not because they have to, but because they choose to. This is great as it’s part of reframing our expectations for retirement. Ideally, you don’t want to work because you are forced into it for financial reasons, but you also don’t want to avoid work opportunities purely because your expectations of retirement exclude those opportunities.

(Taken from Visual Capitalist.)

What does ‘planning ahead’ actually mean to you?

An Aegon 2019 survey says, 25% of global employees say they are on course to achieving their expected retirement income. This is often perceived as meaning: they’ve started early.

But what does ‘early’ mean for you and your personal plan? Planning for retirement even while in your 20s or 30s gives you more time to invest and grow your retirement capital. But that doesn’t mean you can’t start in your 40s. Yes, the later you start certainly poses more challenges, but not if you have other elements in your plan, or it’s part of how you perceive your retirement.

Defining your event horizon (ie. when you would like to retire) is crucial to both your mindset and your investment success. If you start with a positive and personally relevant view of what your retirement (not someone else’s) will look like, you are far more likely to achieve your goals.

How much are you willing to share with your adviser?

Help from a financial adviser has been proven to significantly improve the financial wellbeing of people – both before and after retirement. However, the level at which financial guidance and intervention can help depends on how much you’re willing to share with your financial adviser.

Building a relationship of deep trust, over time, is most often the best way to ensure open and clear communication in a financial planning relationship. Retirement should be enjoyed, not feared!

Effective planning for retirement helps you create expectations that enable you to look forward to retirement.